Page 3 - 2426_Value_Plus_Dec123

P. 3

Monthly Market Roundup Market Outlook: December

The month of November move, however medium to long Going ahead, Indian equity markets will continue

witnessed tumultuous sessions term impact is seen to be positive. to remain volatile this month due to major events

on Dalal Street that was hit by The month finally ended with i.e. Italy referendum on December 4, RBI monetary

double Ds- Donald Trump’s downward bias as S&P BSE policy review on December 7, ECB monetary

victory and Demonetization, thus, Sensex delivering negative return policy on December 8, US Fed meeting outcome

wiping out all the earlier gains of 4.57% to settle at 26652.81 and on December 14 and the development in ongoing

made this year. This surprise Nifty50 lost 4.65% ending the winter session that will be keenly watched

verdict of US elections had month at 8224.50. for market direction. Further, the dollar-rupee

sparked fear in equity markets Realty (-17.63%) and Consumer movement, macroeconomic events, movement

with the 10-year benchmark Durables (-12.75) were the worst in crude oil prices, foreign fund inflows, and

yield soaring to 7.79% from hit sectors during the month. upcoming Q3FY17 corporate earnings are also likely

7.63% m-o-m. FIIs seem to Large chunk of non-banking to affect equity markets. The liquidity concerns

have contributed to this rise, as transactions take place in realty arise from the demonitisation is likely to slow

they sold more than Rs 3,600 sector and real estate prices demand in short term and impact equity markets.

crore in the debt market - their are expected to fall in near We recommend investors that don’t change

biggest outflow since May, on term. Consumer Durables also perception by these short term fluctuations and see

expectations of a possible rate faced negative impact as there market corrections as an opportunity to invest in

hike by the US Fed in December. was a slowdown in spending. fundamentally sound companies.

Modi government’s biggest Meanwhile, the Organization of

crackdown against black money Petroleum Exporting Countries Nifty Technical Outlook: December

revoking legal tender of Rs 500 (OPEC) reached a deal to cut oil

and Rs 1000 notes overnight on production that is expected to Nifty

November 8 left the country in fetch gains to upstream oil, and

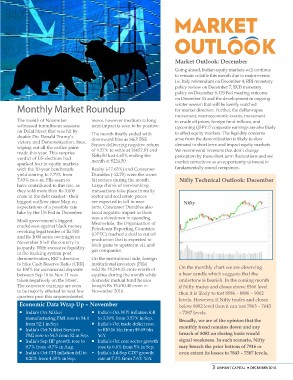

jeopardy. With excessive liquidity gas companies. On the monthly chart we are observing

in the banking system post On the institutional side, foreign a bear candle which suggests that the

demonetization, RBI’s decision institutional investors (FIIs) undertone is bearish. In the coming month

to hike Cash Reserve Ratio (CRR) sold Rs 18,244.25 crore worth of if Nifty trades and closes above 8366 level

to 100% for incremental deposits equities during the month while then it is likely to test 8586 – 8806 – 9062

between Sep 16 to Nov 11 was domestic mutual fund houses levels. However, if Nifty trades and closes

taken negatively on the Street. bought Rs 13,610.40 crore in below 8082 level then it can test 7863 – 7643

The corporate earnings are seen November 2016. – 7387 levels.

to be majorly effected in next few Broadly, we are of the opinion that the

quarters post this unprecedented monthly trend remains down and any

breach of 8082 on closing basis would

Economic Data Wrap Up – November signal weakness. In such scenario, Nifty

may breach the prior bottom of 7916 or

¡ India's Oct Nikkei ¡ India’s Oct WPI inflation fell even extent its losses to 7643 – 7387 levels.

manufacturing PMI rose to 54.4 to 3.39% from 3.57% in Sep. 3 ARIHANT CAPITAL ¡ DECEMBER 2016

from 52.1 in Sep. ¡ India’s Oct trade deficit rose

¡ India’s Oct Nikkei Services to $10.16 bln from $9.69 bln

PMI rose to 54.5 from 52 in Sep. YoY.

¡ India’s Sep IIP growth rose to ¡ India’s Oct core sector growth

0.7% from -0.7% in Aug. rose to 6.6% from 5% in Sep.

¡ India’s Oct CPI inflation fell to • India’s Jul-Sep GDP growth

4.20% from 4.39% in Sep. rate at 7.3% from 7.6% YoY.